Overround: The Bookmaker's Bank Fee

/I was updating the MAFL Fund Performance page last evening and found myself pondering the topic of bookmaker overround.

Overround, you might recall, is the levy that a bookmaker imposes for the privilege of doing business with him (and again I remind you that almost all the bookmakers I know are male, so I make this gender-specific word choice deliberately) and serves as an insurance against inaccuracy in his probability assessments and as a means of generating a guaranteed profit if he's able to balance his book.

When MAFL started out, the TAB Bookmaker routinely embedded 7% or higher overrounds in his Head-to-Head prices but in recent years has felt compelled no doubt by competitive pressures to lower his overround to around 5% or, occasionally, even lower levels. That moves him much more in line with other large, online bookmakers but leaves all of them still levying overround at considerably higher levels than the punter-to-punter-based Betfair website where overrounds often approach 0% (though there, of course, you've transaction fees to cover should you win).

That got me to wondering about how much of MoS' profit in the past couple of years might be attributable to move favourable overrounds and, conversely, how much less the losses in earlier years might have been had MoS been wagering in more punter-friendly waters.

A little maths reveals that the incremental return available to a punter wagering with a bookmaker offering a smaller rather than a larger overround is given by the following:

This equation has four inputs:

- True Probability - this is the actual probability associated with the bet you're making (you can also think of it as the percentage of times you expect to win your wager)

- Bookmaker's Probability - this is the probability used by the bookmaker with whom you're wagering in constructing his price. If the overround he is using is Ov then his price will be 1 / (Bookmaker's Prob x (1 + Ov))

- Smaller Overround - this is the smaller, more favourable overround from a kinder bookmaker

- Larger Overround - this is the larger, less favourable overround from a surlier bookmaker

As an example of the use of this equation consider two bookmakers, one levying 5% overrounds and the other 7% on a proposition they both assess as having a 50% probability. Their prices will therefore be 1/(0.5 * 1.05) or $1.91 for the 5% bookie, and 1/(0.5 * 1.07) or $1.87 for the 7% bookie.

If you land wagers on these teams 60% of the time then the incremental return from using the 5% rather than the 7% bookmaker is 60% / 50% x (7% - 5%)/((1+7%)x(1+5%)) or 2.14%. So, for every $100 you wager you're receiving $2.14 more from the 5% bookie. So, if your ROI with the 7% bookie was 2% you could more than double it by moving to the 5% bookie.

To give you a feel for how this percentage varies depending on the bookmaker's and the true probability, comparing a 5% and a 7% bookmaker, I've created the table below.

The table highlights some of the relationships implicit in the earlier equation, specifically that the incremental return from the 5% bookie is greater for:

- Larger differences between the True and Bookmaker Probabilities

- Smaller Bookmaker Probabilities

- Larger True Probabilities

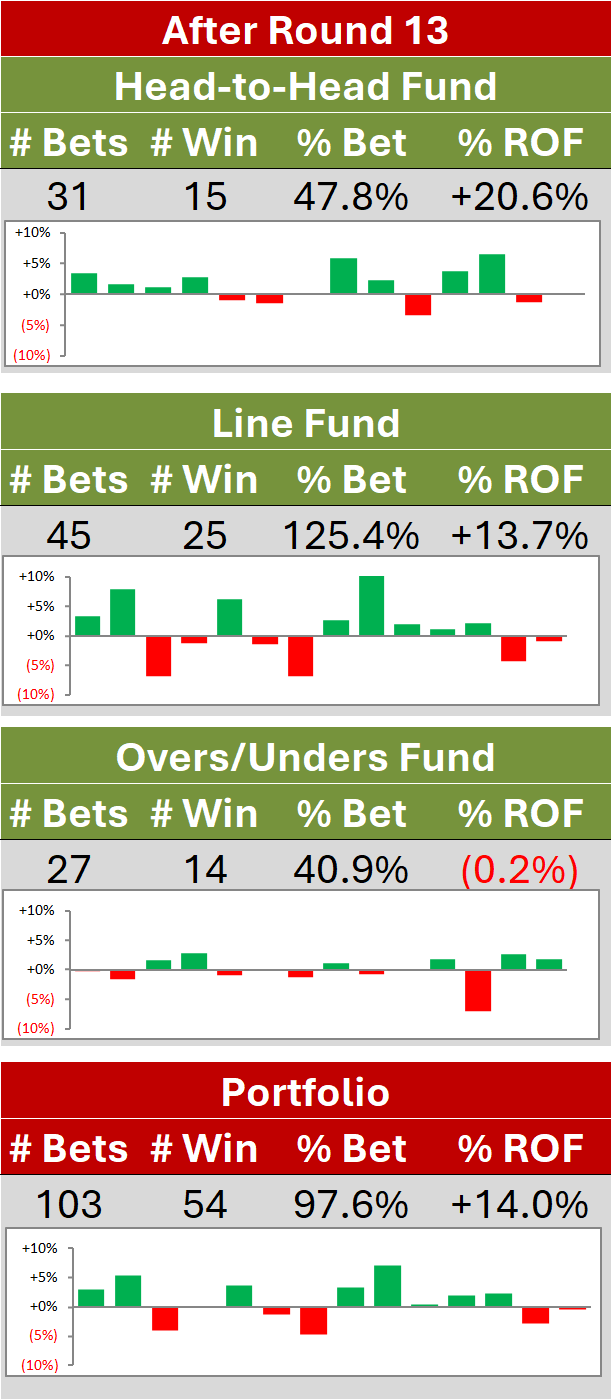

Across the entire history of its wagering MAFL has a (1.4%) ROI. Given this analysis it's not unreasonable to conclude that it could have been at a breakeven level by now had it been wagering with a friendlier bookmaker for more of its history.