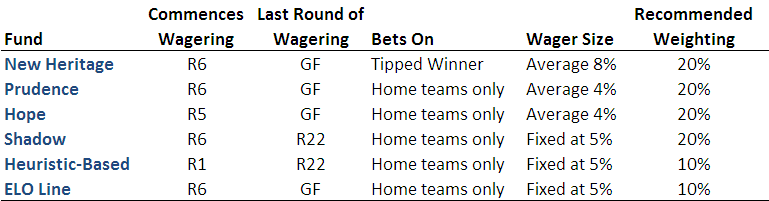

Fund Profiles and Recommended Weightings for 2010

/A few blogs ago (and isn't that a distinctly 21st-century measure of time?) I revealed some details about the six Funds that will be operating this season. Three Funds are backing up from last season on the strength of double-digit returns, while three more are embarking on their rookie wagering seasons.

Two Funds from 2009 have been delisted, the Chi-Squared Fund and the Line Redux Fund, both due to performances that, analysis suggests, were more likely due to intrinsic incompetence than to transient misfortune.

Here's a summary of the six Funds:

Only the new, Heuristic-based Fund will operate from the start of the season, as all other Funds, experience suggests, need four or five rounds of observation before they become sufficiently learned to be entrusted with money.

The Hope Fund will, as it did last year, sit out the first four rounds of the season, and Prudence, New Heritage, Hope, Shadow and ELO-Line will all refrain from betting until Round 6.

All the heuristics we use for tipping - and now for wagering - assume that teams play every week, so they only produce tips for the home-and-away season. As such, the Shadow and Heuristic-based Funds will stop wagering once the finals roll around. All other Funds will continue to wager through to the end of the season.

This year, a pinch of sophistication - though I guess sophistication should really come in soupcons, not pinches - has gone into the determination of Recommended weightings for some of the Funds. Portfolio analysts use a measure called the Sharpe ratio to rate assets. The Sharpe ratio divides an asset's expected return by a measure of the variability of that return. Variability of return represents risk and additional risk needs to be offset by additional expected return. Put another way, assets with larger Sharpe ratios are to be preferred.

The optimal weightings for the New Heritage, Hope and Prudence Funds were derived by calculating (a simplified version of) the Sharpe ratio for portfolios comprising different mixes of these three Funds, using the wagering and game results data for seasons 2006 to 2009. As it turned out, a one-third / one-third / one-third mix was very close to optimal for these three Funds.

Shadow's, ELO-Line's and the Heuristic-based Fund's weightings were determined with, how do I put this, less scientific rigour. I felt happy giving Shadow the same 20% weighting as New Heritage, Hope and Prudence, largely because ... well, because 15% seemed too little and 25% too much (and we did actually identify Shadow as a potential basis for wagering and tracked its performance last season, so it's existence is not purely a manifestation of glorious hindsight).

That left 20% to be shared between the ELO-based and Heuristic-based Funds and, heck, they're both new and they're both speculative, so I assigned them 10% each. (In this respect, MAFL is a bit like most of the disciplines and systems of beliefs I know: thrillingly deep and cogent in its best parts, but discomfitingly shallow in the gaps.)

Anyway, as ever, please feel free to mix your own brew of Funds for your own portfolio. As you now know, your portfolio choices are unlikely to be any less defensible than mine.

Now let's look at each Fund a little more closely.

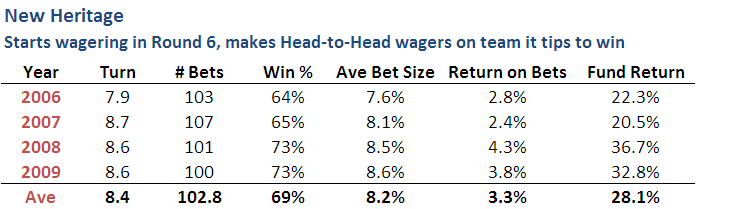

The New Heritage Fund

The New Heritage Fund, you might recall, was conceived as an ironic anti-Fund, the yin to the Heritage Fund's yang.

Last season the Fund performed admirably returning around 30%, a performance that it would have matched or nearly matched in each of the previous 3 seasons had it been in operation. What's more, but for a nasty final four weeks of the regular season last year, the Fund could have produced better than a 70% return.

This Fund has cranked out profits due to a relatively high level of wagering activity - it bets on about 70% of games after Round 5 - and large average bet size allied with a solid ability to pick more than two winners for every loser.

Definitely a keeper, I'd contend.

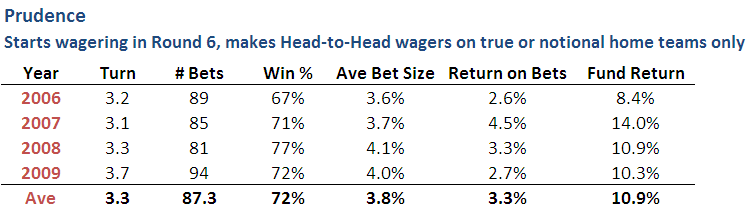

The Prudence Fund

If Prudence played cards it'd look at its hand 4 or 5 times each time before betting and then just bet the minimum. While it'd not make the most of its cards, it'd still grind out a return.

Prudence, on average, bets on about 5 games per round and wagers only about one-half the amount that, on average, New Heritage does. Its win rate is similar to that of New Heritage, so the smaller and fewer wagers it makes translates into consistently lower Fund returns.

Still, an average return of 10% per annum with minimal risk per bet and a four-year unbroken run of profits surely warrants inclusion in anyone's portfolio.

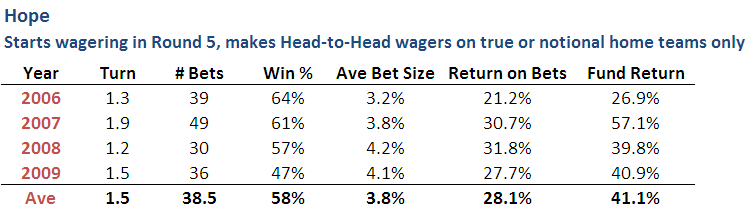

The Hope Fund

The Hope Fund's average wager is about the same size as Prudence's but that's about the extent of the similarities between these two Funds other than that their names are both nouns.

In a typical season Hope will only bet on about one-quarter of the games available to it and these bets will tend to be on teams priced around $3.50 to $4.00. Its average success rate of around 60% is enough to drive its average return to just over 40%, comfortably the highest amongst the three Funds returning from last year.

Last year the Fund's win rate was well below average; a return to trend would be most welcome.

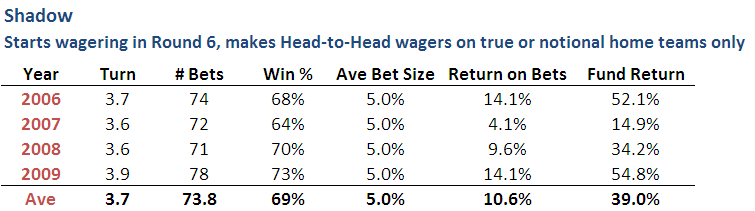

The Shadow Fund

The Shadow Fund can be expected to wager on just over one-half of the games that are available to it and should collect on about 70% of these bets.

Historically it has made returns for entire seasons ranging in size from around 15% to 50% and averaging a little under 40%, partly because its fixed bet size of 5% allows it to convert its win rate into profits.

It is, though, a Fund untested in the wild, so caution should be exercised before approaching it with cash. I suggest you try it on small morsels to begin with.

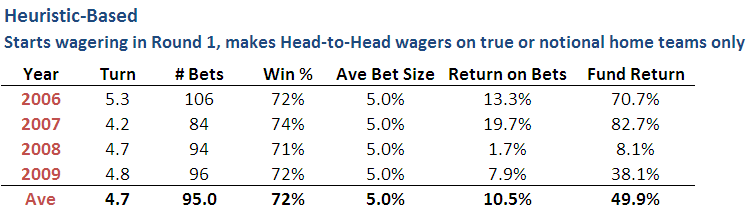

The Heuristic-based Fund

This is a Fund with an ugly, utilitarian name and a complex wagering strategy, so it starts life with a weighty list in the "cons" column. Foremost amongst the "pros", however, is a string of impressive returns and, on this basis alone, it deserves a run this year.

The Fund has a win rate to rival Prudence's, but bets a little more often and a lot more heavily than Pru does, which has resulted in returns of between about 8% and 80% over the past four seasons.

I did explain the Fund's wagering strategy in an earlier blog and I refer you to that posting for more detail and an example, but I'll summarise the philosophy here. The Heuristic-based Fund chooses an heuristic to follow and wagers on that heuristic's tips when it tips the home team until such time as this strategy has caused it to lose money in two successive rounds.

At that point the Fund looks to see which heuristic would have provided the greatest return from wagering on its home team only tips since the start of the season. It then swaps its allegiance to that heuristic, although a swap might actually be a continuation of supporting the current heuristic if that heuristic has the best season-long record despite having lost money in the two most recent rounds. This new heuristic is then followed until such time as it loses for two consecutive rounds, and so on.

To start off proceedings, the Heuristic-based Fund follows Shadow in Rounds 1 and 2.

(Hmmm ... three paras for a description of a Fund's underlying philosophy. No wonder the Fund has a Recommended weighting of just 10%.)

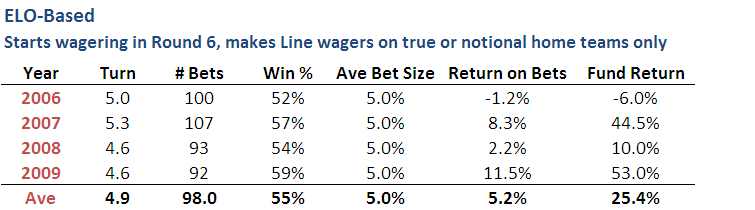

The ELO-based Fund

Another uninspiringly named Fund, though this time without the attraction of an unblemished record of achievement.

The ELO-based Fund uses as its basis the margins of victory derived from my MARS team ratings.

This Fund, when run using data for the past four seasons, bets about as often as the New Heritage Fund, but has a lower win rate, a smaller average bet size but a higher average price per bet. All up this has produced an average Fund return about the same as that of New Heritage but with much more variability, so variable in fact that this Fund would actually have lost money in 2006 had we been using it.

Doubtless, and probably illogically, I'd have felt differently about allowing this Fund to operate this year had that losing season been more recent, but I now profoundly understand how difficult it is to win money wagering on handicap, so I'm willing to overlook this Fund's juvenile record and focus on its more recent successes. (Psychologists have a name for this bias: it's called the Recency Effect and it is said to afflict anyone who puts too much emphasis on recent events or data. Come to think of it, if the best they can come up with as a name for this phenomenon is "Recency Effect" then I don't feel so bad about "Heuristic-based" and "ELO-based".)

*~*~*~*~~*~*~*~*

That the full skinny on all the Funds.

As always, please remember that past performance is no indicator of future returns.