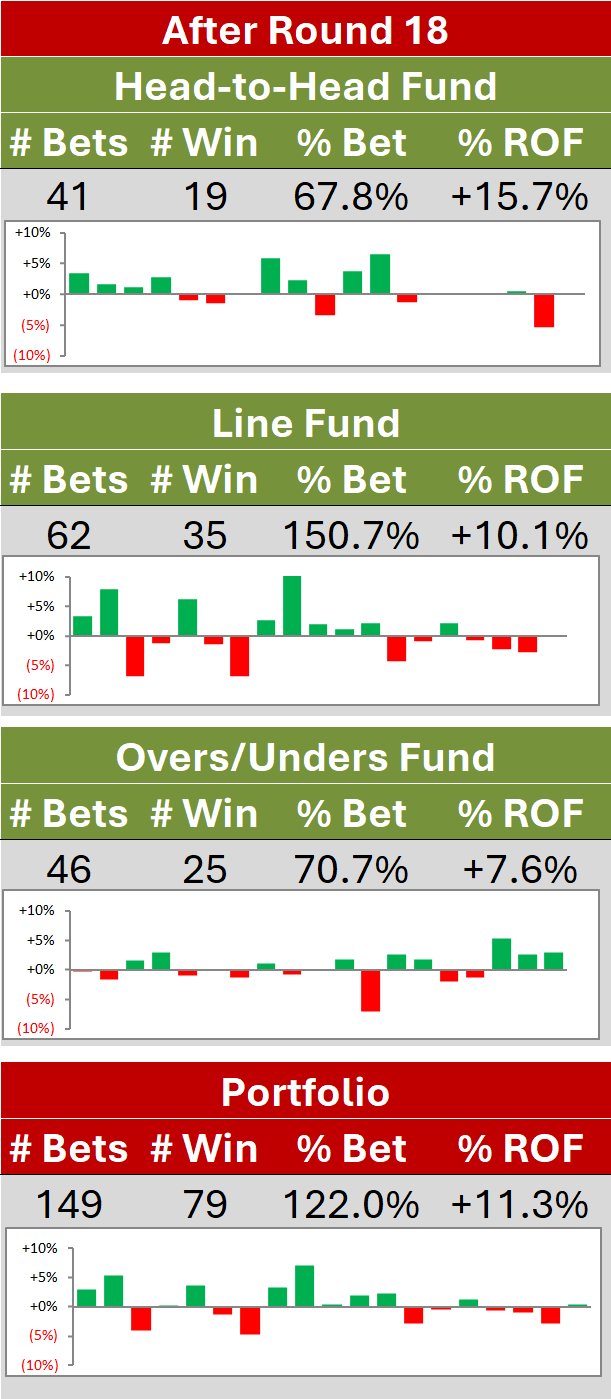

The Head-to-Head Fund and the Risk of Ruin

/Just a quick post tonight in response to an interesting query from an Investor about the 'risk of ruin' of the Head-to-Head Fund. In other words, how likely is it that the Head-to-Head Fund will lose all of the money invested in it before the season's out.

To answer this question I drew upon a statistical technique that's really only been made routine by the widespread availability of significant computing power, the bootstrap. For the current exercise, employing the bootstrap technique required my writing an R script that repeatedly sampled into the historical returns to Head-to-Head Fund wagers across previous seasons, in essence building a series of returns for multiple pseudo-seasons, each 185 games in length. Imagine creating an urn full of balls, each painted with the return from a Head-to-Head wager from any single game from the period 2007 to 2010 - many of them showing 0 for games in which the Head-to-Head Fund chose not to wager - then selecting one ball at a time, noting the return that it showed, returning the ball to the urn, mixing the balls and repeating this selection 185 times.

In constructing the wagering rules for the Head-to-Head Fund one of the decisions I needed to make was what Kelly fraction to employ. The Kelly formula suggests that you should bet an amount equal to (pf - 1)/(f - 1), provided that this positive, where p is your assessment of a team's probability of winning and f is the price on offer. Employing a Kelly fraction of 1, or 'full Kelly', would see you bet this fraction of your entire bankroll In general, this approach leads to larger bets and, if you're right about the edge that your algorithm has, larger profits. But it also increases your risk of ruin, even if you're right about your edge.

My choice for the Head-to-Head Fund is to use a divisor of 5 since my goal is to deliver excitement to Investors, not panic. I thought it'd be interesting to see what effect this choice might have on the stochastic return characteristics of the Fund so, accordingly, I created 100,000 bootstrap seasons for each of the divisors 1 through 6. Also, I thought it'd be interesting to carry out this entire exercise once using the results from seasons 2007 to 2010, then again for the generally more favourable results from seasons 2009 and 2010.

First, consider the upper block of this table, which has been produced by bootstrapping using the results of all games from the 2007, 2008, 2009 and 2010 seasons.

The first row shows that a full Kelly approach would, across a 185 game season, have about a 1-in-4 chance of wiping out the Fund. It would also finish in the red - assuming that it continued to wager in those seasons where it went bust, in some cases returning to profit for the entire season - about 1 season in 7. On average it would produce a 210% return with a standard deviation of about 200%. That's not a level of volatility I could live with, despite the attractive expected return.

As you move down the table you're viewing the results for other divisors and you can see that, as the divisor increases, the risk of ruin declines rapidly, the probability of making a loss remains approximately constant, the expected return declines, and so does the variability of that return. The row for a divisor of 5 is the one that pertains to the Head-to-Head Fund for 2010. (Actually that's not quite true because this season will be a little longer than 185 games, but it's near enough.)

So, if history's any guide, the chances of the Head-to-Head Fund going bust this year are less than 1-in-1,000.

The lower half of the table provides the results for the same scenarios, but this time using only the returns from games in the 2009 and 2010 seasons for bootstrapping.

I'll leave you with a chart summarising the 100,000 replicates for the Kelly Divisor = 5 scenario from the upper half of the table (ie using results for all four seasons).

Despite initial appearances, this distribution is not Normal (it comfortably fails, for example, the Jarque-Bera Test for Normality). It tapers more rapidly than a Normal distribution which, on the downside, reduces the likelihood of an extraordinarily high return, but which also, on the upside, limits the risk of ruin.

(EDIT: I've had a request from one of the MAFL Investors for the Cumulative Distribution Function of the returns for each Kelly Divisor.

Here it is for the bootstraps based on the 2009 and 2010 seasons only:That black line looks very attractive until you realise that:

(a) It's based on an assumption that past returns are a good indicator of future returns

(b) It hides the fact that, using this approach, we'd sometimes be committing 80% of more of the Fund on a single wager and more than the entire Fund over the course of a single round

(c) It also hides the fact that the road to (say) a 50% return might be via a 200% loss saved by a handful of fortuitous wagers at the back end of the season.)